The thought of getting a new car is a real buzz, but figuring out the finance side of things can feel like you’re trying to solve a puzzle. So, how does car finance work, really? Put simply, it’s when a lender gives you the cash to buy a car now, and you agree to pay it back over time with interest. In Australia, this process is well-established, with many options available, particularly in major cities like Sydney and Melbourne for specialised car & asset finance.

Your Simple Guide to Car Finance

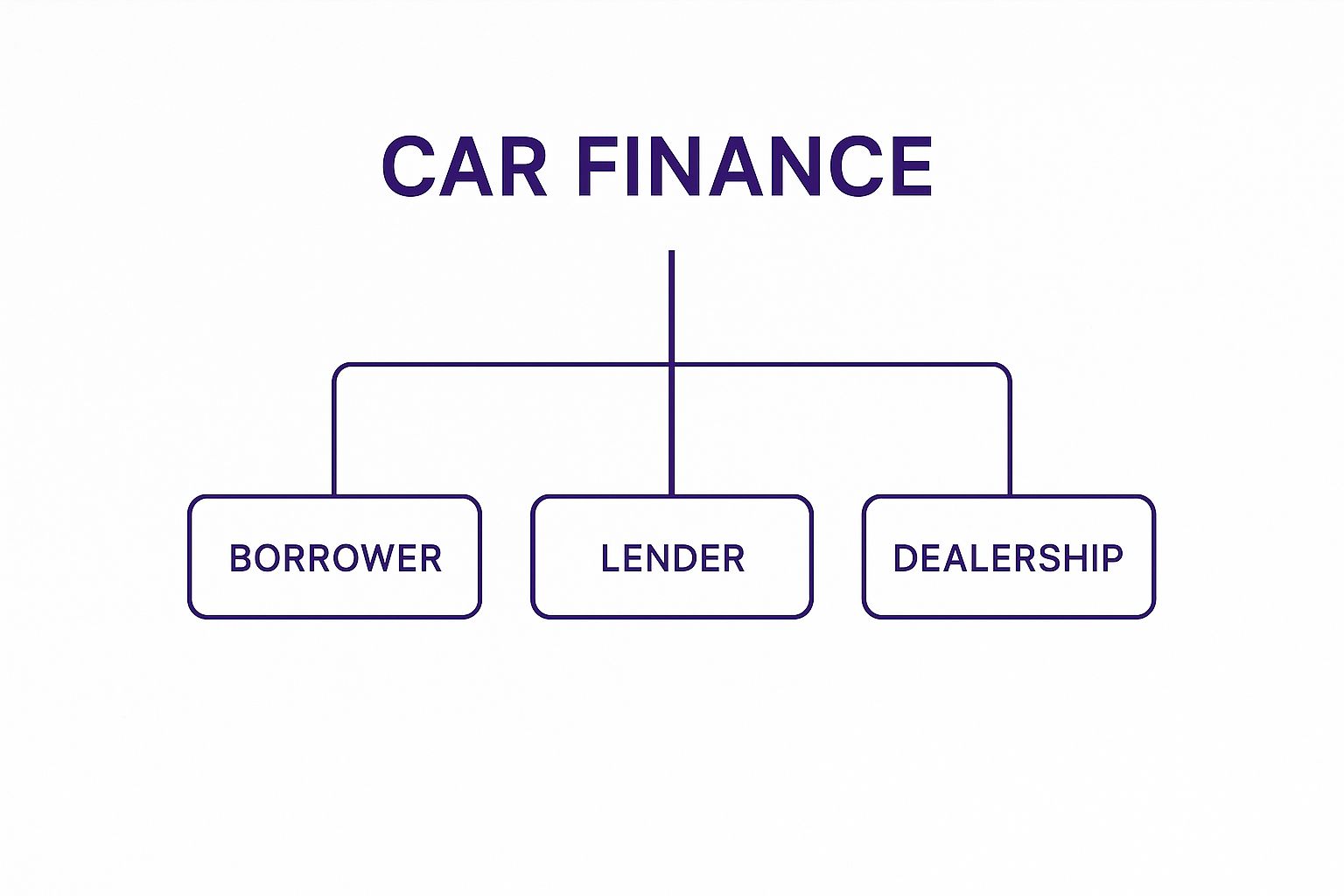

To get your head around car finance, it helps to think of it as a little team effort. There are three main players in the game, and each has a specific role in getting you the keys to your new ride. This relationship is the backbone of pretty much every car loan you’ll find in Australia.

This diagram breaks down how everyone connects in a typical car finance deal.

As you can see, the whole process creates a neat loop between you, your lender, and the person selling the car. Each one is a crucial piece of the puzzle for the finance to get the green light and for the car to officially become yours.

The Key Players in Your Car Loan

First up, there’s you – the borrower. You’re the one who’s found the perfect car and needs the funds to make it happen. Your personal financial situation plays a big part in how much you can borrow and the interest rate you’ll get.

Next, you have the lender. This could be a big bank, a local credit union, or one of the many specialised finance companies you see offering car and asset finance in places like Sydney and Melbourne. Their role is to look at your application, approve the loan, and set up all the repayment details.

And finally, there’s the dealership or private seller. This is the person or business with the car you want to buy. Once your finance is all sorted, the lender usually pays them the money directly, and you get to drive away. Simple as that.

At its heart, car finance is a tool that makes vehicle ownership accessible. It bridges the gap between the car’s price tag and your available cash, enabling you to pay for a significant asset over time rather than all at once.

We’ve designed this guide to walk you through everything, step-by-step, from picking the right loan to making sure you land the best deal possible in Australia.

Exploring Your Car Finance Options in Australia

Alright, now that you’ve got the hang of the basics, let’s dive into the different paths you can take to finance your next car. No two finance agreements are identical, and the best one for you really hinges on your personal situation, your job, and whether the car is for you or your business.

Think of it like planning a road trip. Some routes are direct highways, secured by the car itself. Others are more like scenic detours, offering flexibility but maybe at a different cost. Nailing this choice is how you find a loan that genuinely fits your life and your budget.

And you’re not alone in this. The Aussie vehicle financing market is massive. It was valued at AUD 12,674 billion in 2024 and is expected to rocket to AUD 30,565 billion by 2033. This boom is driven by everything from a hunger for new and used cars to government EV incentives and a new wave of fintech lenders making finance faster and easier. You can read more about the trends shaping Australian vehicle finance on imarcgroup.com.

Secured vs Unsecured Car Loans

For most Aussies buying a car, a secured car loan is the go-to option. It’s pretty straightforward: the car you’re buying acts as security—or collateral—for the loan. This makes it less risky for the lender, and they usually reward you with a lower interest rate.

The trade-off? If you fall behind and can’t make your repayments, the lender has the right to repossess the vehicle to get their money back. It’s the standard, most common way to get into a new set of wheels.

On the flip side, you have an unsecured personal loan. This type of loan doesn’t require any collateral at all. Because the lender is taking on more risk, you’ll almost always face higher interest rates. The big plus here is the freedom—the money is yours to use as you see fit, and the car isn’t legally tied to the loan.

Think of it this way: a secured loan is like using your house as collateral for a mortgage. An unsecured loan is more like a firm handshake deal based on your good name and credit history.

Specialised Finance Routes

Beyond the two main loan types, there are a few other specialised options out there, particularly for employees and businesses.

- Novated Lease: This is a clever three-way deal between you, your employer, and a finance company. Your employer makes the lease payments straight from your pre-tax salary, which can unlock some serious tax savings. It neatly bundles the car’s finance and running costs into a single, simple payment.

- Hire Purchase: A common choice for businesses. With a hire purchase, you’re essentially renting the vehicle from the lender for a set amount of time. You only take full ownership once that final payment is made.

- Chattel Mortgage: This is a heavyweight in the world of car & asset finance for businesses, especially in cities like Sydney and Melbourne. Here, the business buys and owns the vehicle from day one, while the lender takes out a “mortgage” over it as security. Businesses love it for the tax perks, as they can often claim the GST, depreciation, and interest payments.

Each of these paths is designed for a different driver. A novated lease is a fantastic perk for salaried employees, whereas a chattel mortgage is built from the ground up for business owners needing new vehicles or equipment. Getting your head around these differences is the key to making a savvy financial decision.

Decoding the Costs of a Car Loan

Getting a handle on car finance is really about understanding the numbers that make up your loan. It might seem a bit technical at first, but your regular repayment amount really just comes down to three core parts.

Think of it like a recipe. The first ingredient is the principal – that’s just the total amount of money you’re borrowing to buy the car. So, if the car is $30,000 and you put down a $5,000 deposit, your principal is $25,000. Easy.

Next up is the interest rate, which is what the lender charges you for the convenience of borrowing their money. A lower rate is always better, as it means you’ll pay less over the long run. The final piece is the loan term, which is simply how many years you have to pay it all back.

These three elements are constantly working together. For instance, stretching out the loan over a longer term might give you smaller monthly repayments, but you’ll probably pay a lot more in total interest. It’s all about finding a balance that works for your budget.

Looking Beyond the Basics

While principal, interest, and term are the big three, there are a few other key terms you’ll bump into on any loan document, especially here in Australia. Knowing what they mean can save you from nasty surprises later on.

One of the most important is the comparison rate. This is a handy figure that bundles the interest rate with most of the lender’s fees into a single percentage. Its whole purpose is to give you a truer sense of the loan’s total cost.

The comparison rate is your secret weapon for a true apples-for-apples comparison. It stops lenders from hiding hefty fees behind a super-low interest rate, so you get a much more honest picture of what you’ll actually be paying.

You might also come across a balloon payment. This is a significant lump-sum payment that you agree to make right at the end of the loan. It’s a trade-off: your regular repayments will be lower, but you need to have a solid plan for how you’ll cover that big final bill.

Avoiding Financial Surprises

Finally, always ask about early exit fees or early repayment penalties. Some lenders will charge you if you decide to pay your loan off ahead of schedule. Knowing about this upfront gives you the freedom to pay off your debt faster without copping an unexpected fee.

Feeling a bit lost in the numbers? That’s completely normal. A great way to get comfortable is to start playing around with the figures yourself. Using a car loan repayment calculator lets you see exactly how changing the loan term or borrowing amount will affect your repayments. It’s a simple tool that helps you figure out what you can realistically afford before you even start talking to lenders.

Navigating the Car Finance Application Process

Applying for car finance can feel like you’re about to climb a mountain of paperwork, but it’s really just a series of small, manageable steps. When you break it down, what seems like a massive task becomes a pretty straightforward journey—one that puts you firmly in control.

Think of it like getting ready for a job interview. You wouldn’t just turn up and hope for the best, would you? Of course not. You’d get your resume and references in order first. It’s exactly the same idea here.

This practical approach takes the stress out of the equation and gives you a clear roadmap, from browsing cars online to getting the thumbs-up on your loan. So, let’s walk through the exact steps you’ll take, from getting your documents in order to understanding what happens after you hit ‘submit’.

Getting Your Documents Ready

Before you even think about filling out an application form, the smartest thing you can do is gather all your essential paperwork. Lenders need to confirm who you are, how much you earn, and your overall financial situation. Having everything ready to go will make the whole process a whole lot smoother and faster.

It’s really just a standard set of documents to prove you are who you say you are and that you can afford the loan. Getting this sorted is a huge part of understanding how car finance works in the real world in Australia.

Here’s a typical checklist of what you’ll need to have on hand:

- Proof of Identity: Your driver’s licence is a must, and you’ll usually need a second form of ID like a passport or Medicare card.

- Proof of Income: Your two to four most recent payslips will do the trick. If you’re self-employed, you’ll need recent tax returns and maybe your Business Activity Statements (BAS).

- Bank Statements: Lenders will want to see the last three months of your bank statements. This gives them a clear picture of your income, regular expenses, and spending habits.

- Details of Assets and Liabilities: This is just a summary of any other loans, credit cards, or property you might have.

Getting your paperwork organised beforehand is such a simple but powerful step. It shows the lender you’re a serious and organised applicant, which can genuinely help speed things up.

The Lender Assessment

Once your application is submitted, it lands on the desk of the lender’s assessment team. Their job is to go through everything with a fine-tooth comb and decide if you’re a good fit for the loan. Ultimately, they’re looking for evidence that you’re financially responsible and can comfortably handle the repayments.

This is where specialist brokers, like those offering car & asset finance in Sydney or Melbourne, can be a massive help. They have established relationships with lenders, know what each one is looking for, and can frame your application in the best possible light.

The lender will run a credit check to look at your borrowing history and credit score. They’ll also carefully weigh up your income against your expenses to figure out your borrowing capacity. After this review, you’ll get one of three outcomes: unconditional approval (the dream!), conditional approval (they just need a bit more info), or a decline. If it’s a yes, you’ll get the final loan documents to sign, and the funds are usually sent straight to the car dealership or seller within 24 hours.

Financing a New Versus Used Car

So, does it really matter if you’re financing a brand-new car or a trusty second-hand model? In a word: absolutely. A car’s age and history have a huge impact on how lenders see your application, shaping everything from the interest rate they offer to how long you have to pay it off.

Lenders generally see new cars as a safer bet. They have a known market value, no hidden mechanical gremlins, and a full warranty. This gives lenders confidence, which often translates into more competitive, lower interest rates for you. A new car is a predictable asset, and banks love predictability.

On the flip side, financing a used car can sometimes mean copping a slightly higher interest rate. Lenders view them as carrying a bit more risk—the value can be harder to pin down, and there’s always a question mark over potential mechanical issues. Of course, the much lower purchase price of a used car can easily make up for a slightly higher rate.

The Dynamics of New Car Finance

The big thing to get your head around with a new car is depreciation. It’s the unavoidable drop in value that starts the second you drive off the lot. You’re getting the latest tech, that new car smell, and a full warranty, but you’re also financing something that’s losing value faster than anything else you’ll probably ever own.

Even with that in mind, new car finance is incredibly popular, and for some pretty good reasons:

- Promotional Deals: Car brands and their dealerships are always running special finance deals on new models, sometimes with incredibly low or even 0% interest rates.

- Lower Rates: As a rule, lenders save their best rates for new vehicles, which can save you a fair bit of money over the life of the loan.

- Peace of Mind: With a full manufacturer’s warranty, you won’t be blindsided by massive repair bills in the first few years.

Understanding the Used Car Market

Australia has a massive and booming used car market, making it a fantastic option for heaps of buyers. To give you an idea, over 2,074,535 used cars were sold in 2023 alone. Hatchbacks between five and ten years old are especially popular, hitting that sweet spot of affordability and reliability. You can find more data about Australia’s used car financing market on expertmarketresearch.com.

Choosing between new and used isn’t just about the sticker price; it’s about the total cost of ownership. A used car offers a lower entry point, but a new car might provide better long-term value through lower interest rates and maintenance costs.

Ultimately, there’s no single right answer—it all comes down to your personal situation and what you value most. A good finance broker, particularly one who knows the ins and outs of car & asset finance in cities like Sydney or Melbourne, can be a massive help here. They can crunch the numbers on both new and used options to show you exactly what each scenario looks like for your budget.

For more help figuring this out, have a look at our complete guide on the process of car buying in Australia.

Nailing the Best Car Finance Deal for You

Okay, so you’ve got your head around how car finance works. That’s half the battle won. The other half? Making sure you don’t pay a cent more than you have to. Securing a great deal isn’t about luck; it’s about having a solid game plan. This means looking past the first offer that lands in your lap and actively shopping around for the best terms you can find.

Honestly, the smartest move you can make is to get pre-approved for a loan. Think about it: you get your finance sorted before you even start talking to car dealers. When you walk into a dealership with a pre-approved loan, the whole dynamic changes. You’re not just another potential buyer; you’re a cash buyer in their eyes, and that gives you a massive advantage when it comes to negotiating the price of the car.

Don’t Be Afraid to Shop Around

It’s so important to compare offers from a few different places. Don’t just default to your usual bank. Cast a wider net and look at credit unions and specialised brokers, especially those focusing on car & asset finance in major cities like Sydney and Melbourne. Every lender has their own way of assessing things, which means the interest rates and loan terms they offer can be wildly different.

This is great news for you. The car finance market in Australia is packed with lenders all trying to win your business, which forces them to be competitive with their rates and features. The market is always changing, too, with a big push towards financing for electric vehicles as we all move to a greener future. You can actually dive deeper into Australia’s car finance market trends on kenresearch.com.

Getting pre-approval isn’t just about figuring out your budget. It’s about changing the game. You go from being someone asking for a loan to a confident buyer with cash in hand. That simple shift can literally save you thousands.

Your Secret Weapons for a Better Deal

Aside from comparing lenders, there are a couple of other things you can control that will make a huge difference to your overall costs.

- Polish Your Credit Score: Lenders love seeing a strong credit history. It tells them you’re a safe bet. In return for that lower risk, they’ll offer you their sharpest, most competitive interest rates.

- Beef Up Your Deposit: The more money you can put down at the start, the less you’ll need to borrow. A smaller loan means you’ll pay way less interest over the years. Simple as that.

When you pull all these strategies together—getting pre-approved, shopping around, and making the most of your good financial standing—you’re not just a passenger anymore. You’re firmly in the driver’s seat, ready to lock in a fantastic deal.

Answering Your Top Car Finance Questions

Alright, let’s dive into some of the questions that almost everyone asks when they start looking at car finance. Getting these sorted will help you feel much more confident about the whole process.

Can I Still Get a Loan with Bad Credit?

Yes, you absolutely can. It’s a common misconception that a shaky credit history automatically disqualifies you. Many specialist lenders in Australia are more interested in your current situation – your income and financial stability – than just a number on a report. You might find the interest rate is a bit higher to offset the lender’s risk, but there are definitely options out there for you.

What on Earth Is a Balloon Payment?

Think of a balloon payment as a deal you make with the lender. You agree to make a larger, one-off payment right at the end of your loan, and in return, your regular monthly repayments are kept lower. It can be a great strategy if you’re planning to upgrade or sell the car before the loan term is up. Just be sure you have a clear plan for how you’ll cover that final lump sum when the time comes.

How Quickly Can I Get Approved?

You might be surprised at how fast things can move these days. Many lenders and brokers, especially those focused on car & asset finance in major hubs like Sydney and Melbourne, can give you an answer in just a few hours. Once you get the green light, the money can be sorted in as little as 24 hours. You could be driving away much sooner than you think.

Will I Be Penalised for Paying My Loan Off Early?

This one really comes down to the specific lender and loan you choose. Some do charge early exit fees to make up for the interest they’ll lose out on. It’s super important to ask this question directly before you sign anything. That way, you’ll know if you have the freedom to pay the loan off ahead of schedule without getting hit with extra costs.

Getting your head around these common questions is a huge part of understanding how does car finance work in the real world. It takes you from simply knowing the theory to being prepared for the practical side of things.

And don’t forget, once you’ve got your finance sorted and picked out your new ride, the next step is getting it insured. Our guide on finding the right car insurance policy can help you navigate that.

Ready to find a finance solution that’s right for you? The team at LifeX Finance works with over 50 lenders to track down a great deal. Find out more at https://lifex.com.au.